2024 in Review: the year’s most notable Software IPOs and key VC deals with 2025 prediction themes

Exploring the pivotal moments of 2024 and the emerging trends set to define the software and venture capital sectors in the year ahead.

Welcome to my newsletter, Venture Capital & Alii! Today, we turn our attention to the most impactful software IPOs and key VC deals of 2024, analyzing their significance and offering predictions for the trends that will define the year ahead. This is based on my personal perspective. I might miss a few elements — feel free to reach out if you need any additional information.

With the year 2024 now behind us, the software industry solidifies its role as a global engine of innovation and economic growth. This year, marked by a resurgence in software IPOs and record-breaking venture capital investments, underscores the strategic importance of enterprise software, artificial intelligence, and sustainability-driven solutions. Across the industry, IPOs, transformative funding rounds, and cutting-edge technologies defined the landscape. This article delves into the standout IPOs, major venture capital deals, transformative funding rounds, and industry-defining trends that shaped 2024. It also reflects on the challenges ahead and opportunities for future growth.

A resurgent IPO market

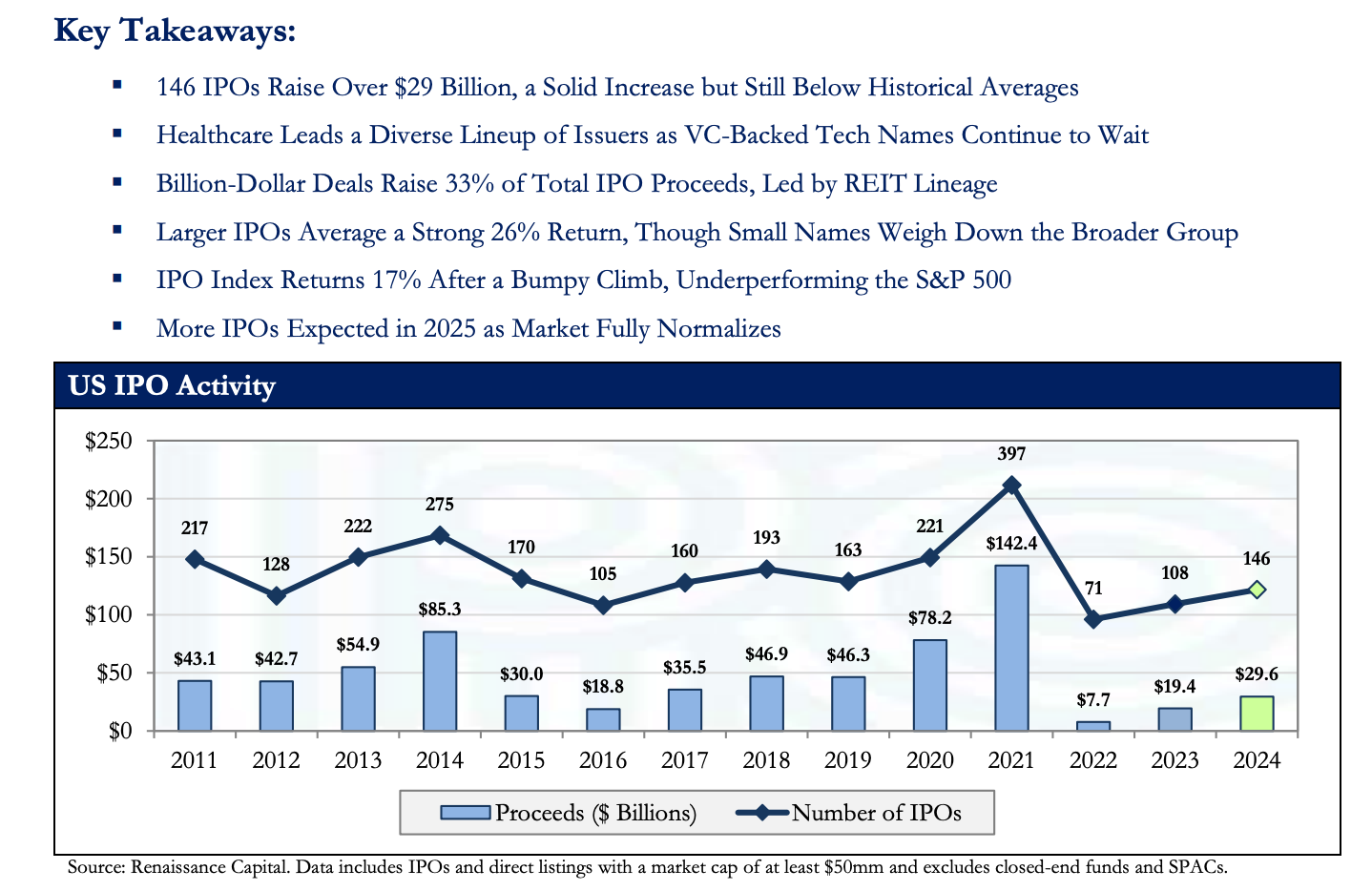

The 2024 IPO landscape experienced a revival, for instance in the US IPO Market with activity increasing by 35% compared to 2023. The year marked an era of innovation, led by enterprise software and AI-powered solutions, as companies capitalized on favorable market conditions to expand their reach.

Reddit, Rubrik, Tempus AI, Astera Labs, and ServiceTitan were at the forefront of this movement. These companies, ranging from AI-driven solutions to cloud data management, demonstrated the growing investor interest in high-growth software firms.

Reddit: from social network to public powerhouse

Reddit, one of the most visited websites globally, had long been anticipated to go public. In 2024, the social media giant debuted on the Nasdaq with a market valuation of approximately $6.5 billion and an initial public offering priced at $34 per share. Known for its user-generated content and community-based discussions, Reddit’s business model revolves around advertising revenue, premium memberships, and a growing e-commerce segment.

Reddit achieved remarkable financial and operational growth in 2024, marked by a 68% increase in revenue, reaching $348.4 million. The company achieved GAAP profitability, with a net income of $29.9 million and a net margin of 8.6%. Operationally, daily active users grew by 47%, totaling 97.2 million, while advertising revenue rose 56% to $315.1 million, reflecting the platform’s appeal to advertisers. International revenue also increased 57% to $60.4 million, signaling success in expanding its global presence.

The company reported a positive operating cash flow of $71.6 million and an adjusted EBITDA of $94.1 million, with a robust margin of 27.0%. Additionally, other revenue streams saw a significant 547% growth, reaching $33.2 million, driven by innovative monetization strategies. Reddit also improved its gross margin to 90.1%, up by 280 basis points from the previous year.

In recent years, Reddit has made strides in monetizing its platform and expanding its user base, which contributed to its strong IPO debut. The IPO comes after years of strategic shifts, including an enhanced focus on advertising products, improved moderation tools, and international expansion. Reddit’s community-driven culture remains a unique selling point, setting it apart from competitors like Twitter and Facebook. Its success in the IPO market highlights investor confidence in platforms with strong user engagement and diversified revenue streams.

Reddit’s journey to the public market is a testament to its adaptability in a competitive landscape, where it has successfully aligned its offerings with advertiser and user needs. With over 430 million monthly active users and a rapidly expanding global footprint, the company’s prospects post-IPO remain promising.

Rubrik: cloud data management pioneer

Rubrik, a leader in cloud data management and data protection, made its long-awaited public debut in 2024 with an IPO valuation of approximately $6.6 billion and shares priced at $32 per share. Founded in 2013, Rubrik specializes in providing enterprises with a single platform for managing data backups, recovery, and governance across hybrid and multi-cloud environments.

Rubrik’s IPO follows years of consistent growth fueled by an increasing reliance on cloud computing and stricter regulatory demands for data security and compliance.

The company's ability to address both operational resilience and cybersecurity challenges has made it indispensable for industries such as finance, healthcare, and government.

Rubrik delivered a strong financial performance in Q3 2024, with revenue growing by 43% to $236.2 million, exceeding the $217.5 million estimate. The company reported a reduced loss per share of 21 cents, outperforming Wall Street’s projected loss of 40 cents per share. Rubrik also achieved a significant milestone, reporting $1 billion in annual recurring revenue (ARR) from subscriptions, with net new ARR of $83 million, surpassing the consensus of $58 million.

Following its successful IPO in April 2024, which raised over $750 million with an initial share price of $32, the company’s stock has surged by more than 20% post-earnings announcement, reaching $64.51 in early trading.

Key to Rubrik's success is its focus on simplifying data management through AI and automation, which reduces operational overhead for IT teams while improving recovery speeds. Its strategic partnerships with Microsoft Azure and AWS, combined with an expanding customer base that includes Fortune 500 companies, solidified investor confidence. Rubrik’s IPO success highlights the market’s appetite for companies solving complex enterprise data challenges in an increasingly digital world.

Tempus AI: revolutionizing precision medicine

Tempus AI, a trailblazer in AI-driven healthcare solutions, entered the public markets in 2024 with a market valuation of $6.1 billion and an IPO price of $37 per share. Founded in 2015, the company leverages artificial intelligence to analyze molecular and clinical data, enabling doctors to provide precision treatments for complex diseases like cancer.

Tempus’ platform integrates genomics, imaging, and patient histories into actionable insights that help healthcare providers personalize treatment plans. By bridging the gap between vast data repositories and real-time clinical decisions, Tempus is at the forefront of revolutionizing healthcare delivery.

Tempus AI demonstrated robust financial performance in Q3 2024, with a 33% increase in revenue, reaching $180.9 million. Despite this growth, the company reported a net loss of $75.8 million, which included $22.2 million in stock-based compensation and related taxes. A key highlight was the 64.4% year-over-year growth in data services revenue, underscoring the strength of its data-driven offerings. Additionally, Tempus announced the acquisition of Ambry Genetics for $375 million in cash and $225 million in stock, further expanding its capabilities. For the full year 2024, Tempus projects total revenue of approximately $700 million, reflecting an annual growth rate of 32%.

The company's successful IPO was underpinned by its rapid revenue growth and a network of partnerships with leading hospitals, pharmaceutical companies, and research institutions. With the global healthcare sector increasingly reliant on AI to improve outcomes and reduce costs, Tempus AI’s public debut marks a significant milestone for AI applications in medicine.

Moving forward, Tempus plans to expand its platform to address new areas in predictive diagnostics and preventative care, unlocking further value for its stakeholders.

Astera Labs: enabling the next generation of semiconductor innovation

Astera Labs, a cutting-edge semiconductor company, went public in 2024 with a $6 billion valuation and an initial share price of $26. Specializing in connectivity solutions for data-centric systems, Astera Labs plays a pivotal role in powering AI, cloud computing, and high-performance computing workloads.

The company’s focus on developing silicon solutions for PCIe, CXL, and Ethernet connectivity has positioned it as a critical enabler of next-generation technologies. Its products are used in data centers, 5G networks, and autonomous vehicles, industries that require unparalleled speed and reliability in data processing.

Astera Labs delivered record-breaking results in Q3 FY2024, with revenue reaching $113.1 million, reflecting a 47% quarter-over-quarter growth and an impressive 206% year-over-year increase. The company achieved strong profitability metrics, posting a GAAP gross margin of 77.7% and a non-GAAP gross margin of 77.8%, demonstrating efficient cost management. Despite this growth, Astera Labs reported a GAAP net loss of $7.6 million, consistent with the prior year, alongside a GAAP operating loss of $8.9 million, resulting in a -7.9% operating margin. However, on a non-GAAP basis, the company achieved an operating income of $36.6 million, with a 32.4% operating margin, and reported a non-GAAP earnings per share (EPS) of $0.23, surpassing the GAAP loss per share of $0.05.

Astera Labs exceeded analyst expectations, with revenue coming in 16% higher than forecasted and EPS outperforming projections by 28%. Following these results, the company’s stock surged by over 18%. Looking ahead, Astera Labs anticipates Q4 FY2024 revenue between $126 million and $130 million, with an expected gross margin of approximately 75%. While the company’s strong growth and financial outperformance are noteworthy, ongoing net losses highlight the need for continued focus on improving profitability.

Astera Labs’ IPO reflects the surging demand for semiconductor innovations that address the bandwidth and latency challenges of modern digital infrastructures. Its impressive growth trajectory and strategic collaborations with cloud providers and OEMs ensured strong investor interest. The IPO underscores the importance of semiconductor companies in the rapidly evolving tech landscape.

Astera Labs plans to use proceeds from its IPO to accelerate R&D efforts, ensuring it remains at the forefront of semiconductor innovation as AI workloads grow more demanding.

ServiceTitan: The SaaS Powerhouse for Trades Industries

ServiceTitan, a SaaS leader revolutionizing the home services industry, went public in december 2024 with a valuation of $9.5 billion and shares priced at $71 (opened at $101). Founded in 2012, ServiceTitan provides software solutions to help HVAC, plumbing, electrical, and other trades businesses optimize their operations.

The platform integrates scheduling, dispatch, invoicing, marketing, and customer management into a comprehensive solution that enhances efficiency and profitability for service providers. By digitizing traditionally manual processes, ServiceTitan has become an essential tool for contractors navigating an increasingly competitive marketplace.

ServiceTitan reported solid revenue growth in 2024, with total revenue increasing by 31% year-over-year to $614.3 million, driven by its platform subscriptions and usage-based fees, which accounted for 95% of total revenue. The company’s FinTech products generated $28.9 million, reflecting a 26% growth, while professional services contributed 5% of overall revenue.

Despite this growth, ServiceTitan recorded a net loss of $195 million for the year and struggled with profitability metrics. Its non-GAAP operating margin stood at 2%, significantly below the industry median of 15%, and gross margins were 70%, trailing the Meritech Software Index median of 78%.

Furthermore, its free cash flow margins were negative at -2%, in sharp contrast to the industry median of 15%. The company’s implied ARR reached $772 million, marking a 24% increase year-over-year.

ServiceTitan’s IPO success reflects the growing importance of SaaS solutions in traditionally underserved industries. Its rapid expansion, strong customer retention, and strategic acquisitions have reinforced its leadership in the trades sector. As the demand for digital transformation accelerates across industries, ServiceTitan is well-positioned to drive continued growth in the post-IPO era.

The company’s next phase of growth will likely focus on global expansion and deepening its AI-driven automation capabilities to further simplify operations for its clients.

The thriving landscape of Venture Capital in enterprise software: key 2024 highlights

The year 2024 witnessed a surge in VC activity, particularly in the enterprise software sector. This influx of capital underscores investors’ growing confidence in innovative solutions that address pressing business needs. Companies like HR Path, Pigment, Planhat, and Dcycle emerged as prominent beneficiaries of this trend, each leveraging their funding rounds to scale operations, enhance product offerings, and consolidate market positions. Below, we delve into the specifics of their funding journeys and the strategic directions enabled by these investments.

HR Path: advancing global HR solutions

HR Path, a global leader in human resources consulting and solutions, made headlines in mid-2024 by securing a record €500 million (approximately $537 million) in financing from Ardian, one of the world’s leading private investment houses. Founded in 2001, HR Path provides comprehensive HR services, including consulting, system implementation, and payroll outsourcing. This funding represents a major milestone for the company as it positions itself as a "one-stop shop for HR."

The fresh capital is set to accelerate HR Path’s international expansion, particularly in key markets like the United States, Canada, Germany, the Nordic countries, and Australia. Currently operating in 22 countries, the company serves over 3,000 clients globally with a workforce exceeding 1,800 employees. Its turnover of €215 million and CAGR of 25% since 2021 reflect its consistent growth trajectory. This funding will also facilitate further acquisitions, enabling HR Path to consolidate its position as a leader in HR transformations.

Pigment: redefining business planning

Paris-based startup Pigment has rapidly emerged as a disruptor in the business planning software market. In April 2024, Pigment announced a $145 million Series D funding round led by ICONIQ Growth. Founded in 2019, Pigment offers a cutting-edge platform that integrates data to streamline financial and operational planning. This innovation enables companies to make real-time, data-driven decisions.

The company’s recent funding follows an impressive period of growth, marked by a tenfold increase in its user base over the past year. Notable clients, including Klarna, Miro, and Airtable, have adopted its platform. Pigment plans to use this funding to expand its presence in North America, intensify investment in artificial intelligence capabilities, and broaden the scope of its product use cases. These strategic moves position Pigment as a key player in the increasingly competitive business planning sector.

Planhat: enhancing customer success management

Planhat, a customer success platform headquartered in Stockholm, closed a $50 million Series A funding round in 2024. Since its founding in 2014, the company has developed tools to help businesses manage renewals, reduce customer churn, and identify opportunities for upselling and cross-selling. With over 1,000 customers globally, Planhat has become an essential tool for SaaS companies aiming to optimize customer retention and growth.

In 2024, Planhat’s revenue reached $33 million, reflecting its growing influence in the customer success management space.

The recent funding is expected to fuel further development of its platform and support market expansion efforts. By focusing on enhancing its AI-driven analytics and predictive insights, Planhat aims to solidify its position as a leader in the rapidly evolving customer success market.

Dcycle: empowering sustainable business practices

Dcycle, a Madrid-based sustainability tech startup, has captured the attention of investors with its innovative approach to environmental impact management. In 2024, Dcycle has raised €6 million in a Series A funding round to expand its platform’s capabilities and drive growth in the sustainability space. The platform offers businesses the tools to measure, analyze, and improve their sustainability metrics, enabling compliance with evolving environmental regulations and meeting consumer expectations for eco-conscious practices.

Dcycle’s user-friendly software integrates seamlessly with existing business processes, allowing companies to track carbon emissions, manage supply chain sustainability, and assess the lifecycle impact of their products. With sustainability becoming a top priority for businesses globally, Dcycle is well-positioned to address the rising demand for actionable environmental data and analytics.

As the enterprise software industry continues to evolve, these funding milestones not only underscore investor confidence but also pave the way for groundbreaking advancements. By scaling their operations, enhancing their product offerings, and entering new markets, these companies are set to redefine their respective domains and deliver lasting value to stakeholders.

Prediction themes shaping the software industry for 2025

As the software sector continue its strong evolution, 2025 promises to usher in transformative changes driven by technological innovation, shifting user expectations, and heightened competitive pressures. These developments signal a pivotal moment for the industry, as businesses leverage new capabilities to enhance efficiency, address emerging challenges, and unlock growth opportunities. This analysis delves into five critical themes shaping this dynamic landscape, offering an in-depth exploration of their implications for stakeholders across the ecosystem.

1. Artificial Intelligence and Machine Learning: the cornerstone of innovation

AI and ML have transitioned from being optional enhancements to essential components of SaaS platforms. In 2024, 92% of SaaS business were expected to embed AI-driven functionalities, fundamentally reshaping decision-making processes and customer interactions.

The integration of AI is especially transformative in domains like CRM, where it predicts user behaviors and optimizes engagement strategies. Similarly, in data analytics, ML algorithms deliver real-time insights, allowing businesses to make data-informed decisions. Key advancements, such as natural language processing (NLP) and computer vision, are broadening the scope of software applications across industries. AI's pervasiveness reflects its evolution from a feature to a foundational pillar of modern SaaS platforms, offering unparalleled operational efficiencies and competitive advantages.

Moreover, the rise of generative AI, with applications in content creation, software debugging, and marketing automation, signals a new era of innovation. Companies like OpenAI and Google (Gemini) or Mistral AI are leading the charge, ensuring that AI capabilities are not only accessible but also deeply integrated into everyday business workflows.

2. Vertical SaaS: tailored solutions for specialized needs

Vertical SaaS represents a paradigm shift from generalized solutions to industry-specific platforms, addressing unique operational requirements and compliance needs. Industries such as healthcare, real estate, and manufacturing are witnessing an influx of tailored tools that enhance efficiency while adhering to sectoral regulations.

Notable players like Veeva Systems in life sciences and Procore in construction management underscore the success of vertical SaaS. These platforms integrate industry-specific workflows, metrics, and automation, streamlining operations and driving value.

Emerging markets, too, are fertile ground for vertical SaaS growth. Startups focusing on agriculture, education, and renewable energy are leveraging tailored solutions to address localized challenges. This trend underscores the increasing importance of customization and specialization in software development.

3. Enhanced Security: meeting the rising threat landscape

As cyberattacks grow more sophisticated, SaaS providers are intensifying their focus on robust security frameworks. Enhanced encryption protocols, multi-factor authentication, and AI-driven threat detection are becoming standard practices to safeguard user data and comply with global privacy regulations such as GDPR and CCPA.

Innovations in zero-trust architectures, decentralized identity solutions, and blockchain-based security frameworks are also gaining momentum. Analysts predict that the global cybersecurity market for SaaS will surpass $562.72 billion by 2032, underscoring the critical demand for advanced security measures.

Notably, the rise of edge computing and IoT integration has introduced new vulnerabilities, prompting SaaS companies to adopt proactive monitoring and regular security audits. By prioritizing security, providers not only mitigate risks but also build trust with users, which is increasingly becoming a competitive differentiator.

4. Micro SaaS: niche markets and agile solutions

Micro SaaS, characterized by highly specialized solutions targeting specific pain points, is gaining traction among independent developers and small teams. These products, often single-function applications or browser extensions, require minimal investment while addressing niche market needs effectively.

The rise of the creator economy has further fueled this trend, enabling individuals to monetize bespoke digital products. Micro SaaS aligns with the broader demand for hyper-specialization, agility, and cost-efficiency. By catering to underserved segments, it provides a pathway for innovation in markets overlooked by larger players.

Additionally, platforms supporting micro SaaS development—such as Shopify for e-commerce plugins and Notion for workflow enhancements—are fostering ecosystems that empower developers. This trend not only democratizes software innovation but also promotes sustainability through lean operational models.

5. Low-Code and No-Code platforms: accelerating democratized development

Low-code and no-code platforms are revolutionizing software development by enabling users with minimal technical expertise to build functional applications. These tools significantly reduce development costs and time-to-market, making them particularly appealing to startups and SMEs.

Leading platforms like OutSystems, Bubble, and Mendix are at the forefront of this movement. With a projected CAGR of 28% through 2028, low-code/no-code technologies are poised to redefine software delivery.

Beyond startups, enterprises are increasingly adopting these platforms to accelerate internal application development and foster innovation. The integration of AI into low-code environments further enhances their capabilities, enabling automated code generation, real-time debugging, and seamless scalability.

Conclusion

The software industry in 2024 showcased its resilience and capacity for transformation. High-profile IPOs and key VC deals underscored its role in driving innovation and addressing global challenges. As enterprises increasingly adopt AI, prioritize sustainability, and embrace niche software solutions, the path forward appears bright. However, navigating an uncertain economic and regulatory landscape will require agility and strategic foresight. The lessons of 2024 will undoubtedly influence the industry’s future, solidifying software’s place at the heart of global progress.

Thank you for reading this article! What specific topics in VC or regarding software would you be interested in? Feel free to share your feedback 🌐 and give a ❤️ if you enjoyed it!